Online Order

Online OrderArticle Guidance

Off payments towards land can differ commonly, that may succeed tough to know the way far you may need to keep. not, while happy to get property, there are numerous minimum downpayment direction to adhere to. Here’s what you have to know before making a downpayment into a house.

An advance payment was money that you pay initial towards the a household get. In addition, it represents their first possession risk at your home. Generally, its conveyed as the a percentage of the complete price. Like, an effective ten% deposit toward an excellent $400,000 home is $40,000.

Before you go to acquire a house, you will probably want to make a downpayment. Your lender will then make it easier to money with the rest of the brand new purchase price in the form of a mortgage loan .

You will loans in Marion find some mortgage apps that make it you’ll be able to to help you pick property no money down , but not, which we are going to shelter later.

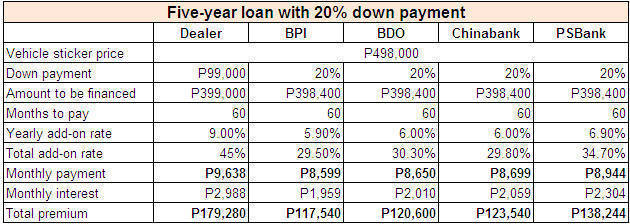

To make good 20% down-payment had previously been felt new standard for buying property, these days, it is simply a standard one loan providers use to determine if you would like home loan insurance coverage. Usually from thumb, for individuals who establish less than 20% on a conventional loan , lenders will require one bring individual home loan insurance coverage (PMI) .

Thankfully, you don’t need to make you to large from an advance payment purchasing a home in today’s was only 8% getting first-day homeowners , based on data on the National Association off Realtors (NAR). For repeat buyers, the typical was 19%.

Homeowners will get mistake exactly how much they have to set out on the a beneficial house or apartment with minimal requirements place because of the loan providers. The brand new table less than also provides a quick look at the lowest matter needed for per financing program.

Traditional funds: 3% down-payment

Specific conventional loan applications, like the Federal national mortgage association HomeReady mortgage and you will Freddie Mac House Possible financing , allow for down payments as little as step 3%, provided you satisfy specific earnings restrictions.

you will you prefer a somewhat high credit history. The new HomeReady financing means the absolute minimum 620 rating, as the Family You are able to loan requests about a beneficial 660 rating.

FHA loans: step 3.5% down-payment

You might shell out as little as 3.5% down that have financing backed by the newest Federal Houses Government (FHA) – when you have at the least a 580 credit rating. This new deposit minimum with the an FHA mortgage jumps to ten% if your credit rating was between 500 and 579.

Virtual assistant financing: 0% deposit

Qualified army provider professionals, experts and you can surviving spouses will get a loan guaranteed because of the You.S. Department out-of Experts Points (VA) which have 0% down. While there’s absolutely no necessary minimal credit history to own a beneficial Virtual assistant financing , of a lot loan providers could possibly get impose their own qualifying requirements.

USDA money: 0% down-payment

The fresh You.S. Company away from Agriculture (USDA) offers 0% down payment home loans so you’re able to qualified reasonable- and moderate-income homebuyers into the designated rural section. There’s no minimal credit score necessary for good USDA mortgage , but the majority lenders anticipate to find about a good 640 score.

Jumbo financing try loans which can be larger than the newest compliant loan limitations lay by Federal Homes Loans Department (FHFA). Due to their proportions, these types of money can’t be protected because of the Federal national mortgage association and you may Freddie Mac , the 2 providers that provides financial support for many lenders.

This is why, these funds are believed riskier to have loan providers, therefore you can easily will you want more substantial deposit to-be accepted.

Like any economic decision, while making a massive advance payment has its advantages and disadvantages. Here’s a look at what you should believe before you going.

Lower desire costs: As the you’re borrowing from the bank less order your family, possible spend down attention charge along the longevity of the loan. As well, loan providers may give your a much better interest since the they’re going to see your because a quicker high-risk debtor.

Alot more guarantee: Your property security is the percentage of your residence which you very own outright. It is counted by your residence’s newest value minus the amount you are obligated to pay on your own financial. The more collateral you’ve got , the greater amount of you could control this asset.

Less cash on hand: And also make a bigger down-payment often means you have less overall offered to create fixes or satisfy almost every other financial specifications, such as for instance building a crisis fund or coating needed home fixes.

Extended time and energy to save yourself: Getting off 20% can indicate that the deals mission is quite higher. Thus, it can take extended to be a homeowner than if you produced an inferior deposit.

Long-term professionals: Some of the advantages of and work out a more impressive downpayment are supposed to give you a hand ultimately. If you aren’t thinking of located in our home getting good while, you will possibly not benefit as much.

How much if you set-out towards property?

Regrettably, there’s no one to-size-fits-all of the means to fix how much cash their downpayment would be. It does rely on the fresh new information on your debts. After all, while you are there are numerous advantageous assets to to make more substantial downpayment, paying a lot of initial to possess a property you will make you feel house-bad and you can not able to subscribe your almost every other financial requirements.

You should fuss with assorted down payment circumstances up to your land to your one that feels most comfortable for you. Whenever you are only getting started exploring the way to homeownership, our house affordability calculator helps you determine what down-payment is right for you.